How Institutional Portfolios Actually Allocate Capital

Most investors think portfolio construction begins with a simple question:

What should I buy?

Serious allocators usually start somewhere else.

They ask what the portfolio is trying to achieve, what risks it can tolerate, which exposures it needs, and how capital should be allocated across those exposures under the current environment.

That difference matters.

A portfolio is not just a collection of assets. It is a structure of exposures, roles, assumptions, and risks.

Many individual portfolios are built from preferences. A stock they like. An ETF that performed well. An asset class that sounds defensive. A theme that feels compelling.

But owning an asset is not the same as understanding what job it is doing.

Institutional portfolio construction is not perfect. Institutions can be wrong, crowded, slow, or overconfident. But the process is usually more structural than the way most individuals allocate capital.

The lesson is not that investors should blindly copy institutions.

The lesson is that serious portfolio construction starts with structure, not stories.

How Most Individuals Think About Allocation

Many self-directed investors build portfolios from the bottom up.

They begin with attractive assets, familiar names, or convincing narratives.

A position is added because:

the company seems strong

the ETF feels diversified

the asset has performed well

the valuation looks attractive

the theme sounds compelling

the macro story feels persuasive

This is understandable.

Markets are usually presented through stories. Financial media discusses individual securities, sectors, themes, and predictions. Platforms make it easy to buy exposure before defining why it belongs in the total portfolio.

The problem is not that these ideas are always wrong.

The problem is that they often enter the portfolio without a defined role.

An investor may own equities, bonds, gold, commodities, cash, and several thematic ETFs, then assume the portfolio is diversified because it contains multiple holdings.

But diversification is not a holdings count.

A portfolio with many assets can still depend on the same macro driver. A portfolio with several ETFs can still be concentrated in growth, liquidity, duration, or inflation sensitivity.

When allocation is treated as a secondary step, the portfolio becomes a collection of views rather than a deliberate structure.

That is where fragility begins.

How Institutional Portfolios Actually Think

Institutional portfolios usually begin with a different set of questions.

Not:

What do we like?

But:

What is this portfolio designed to do?

What return objective is required?

What level of drawdown is tolerable?

What liquidity is needed?

What constraints apply?

Which risks are acceptable?

Which risks must be controlled?

How should the portfolio behave in different environments?

This is the core difference.

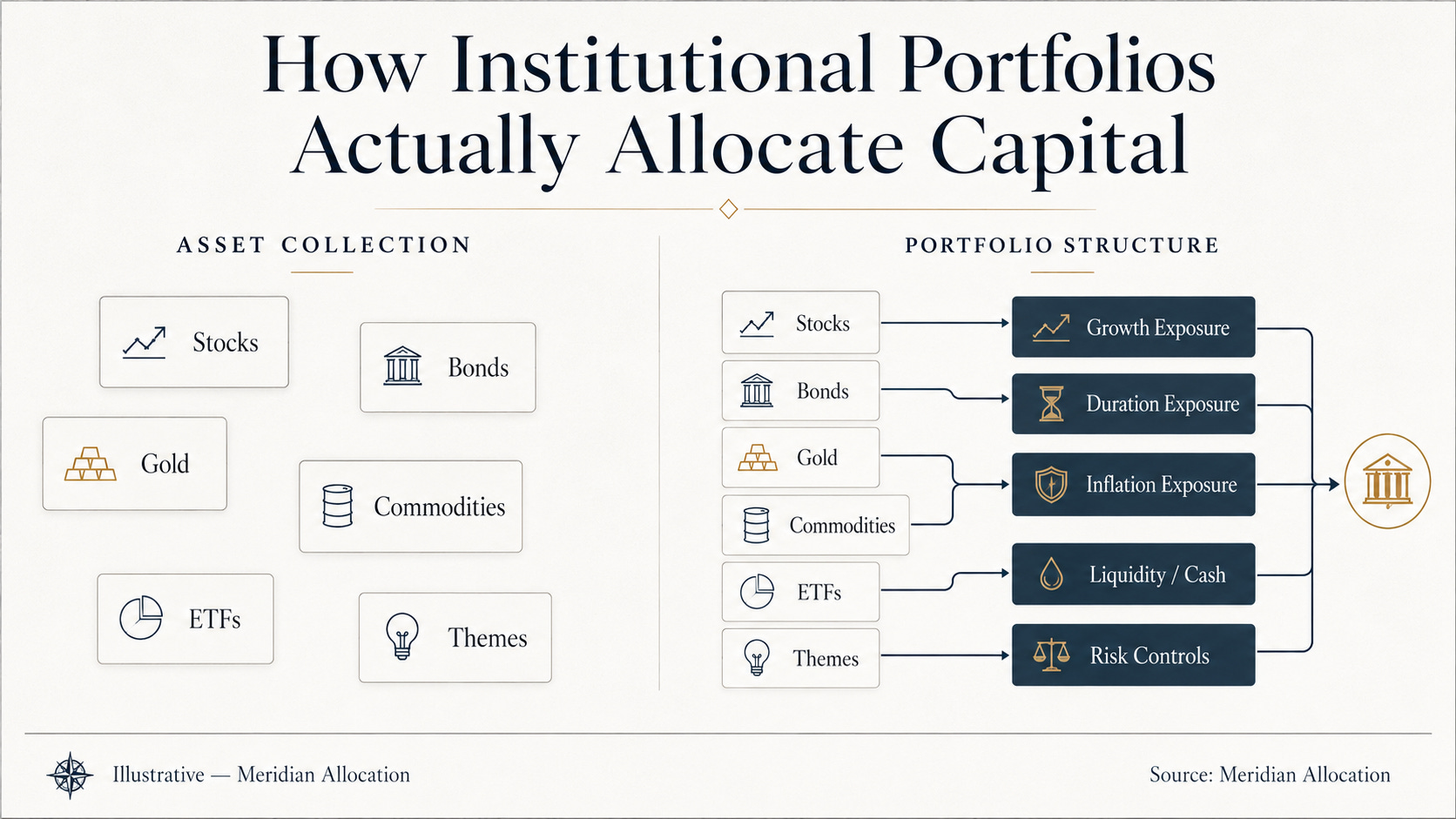

Institutional allocation is usually designed at the total portfolio level.

Individual assets matter, but they are not assessed only on standalone appeal. They are assessed by how they change the behaviour of the entire portfolio.

A holding is not just a holding.

It is a source of exposure.

It may add growth sensitivity, duration sensitivity, inflation sensitivity, liquidity, volatility reduction, or hidden concentration.

It may appear diversifying in one regime and become fragile in another.

The institutional allocator is not simply asking whether an asset is good.

They are asking what the asset does to the portfolio.

That is a higher-quality question.

Capital Allocation Is Really Exposure Allocation

At the institutional level, capital allocation is usually exposure allocation.

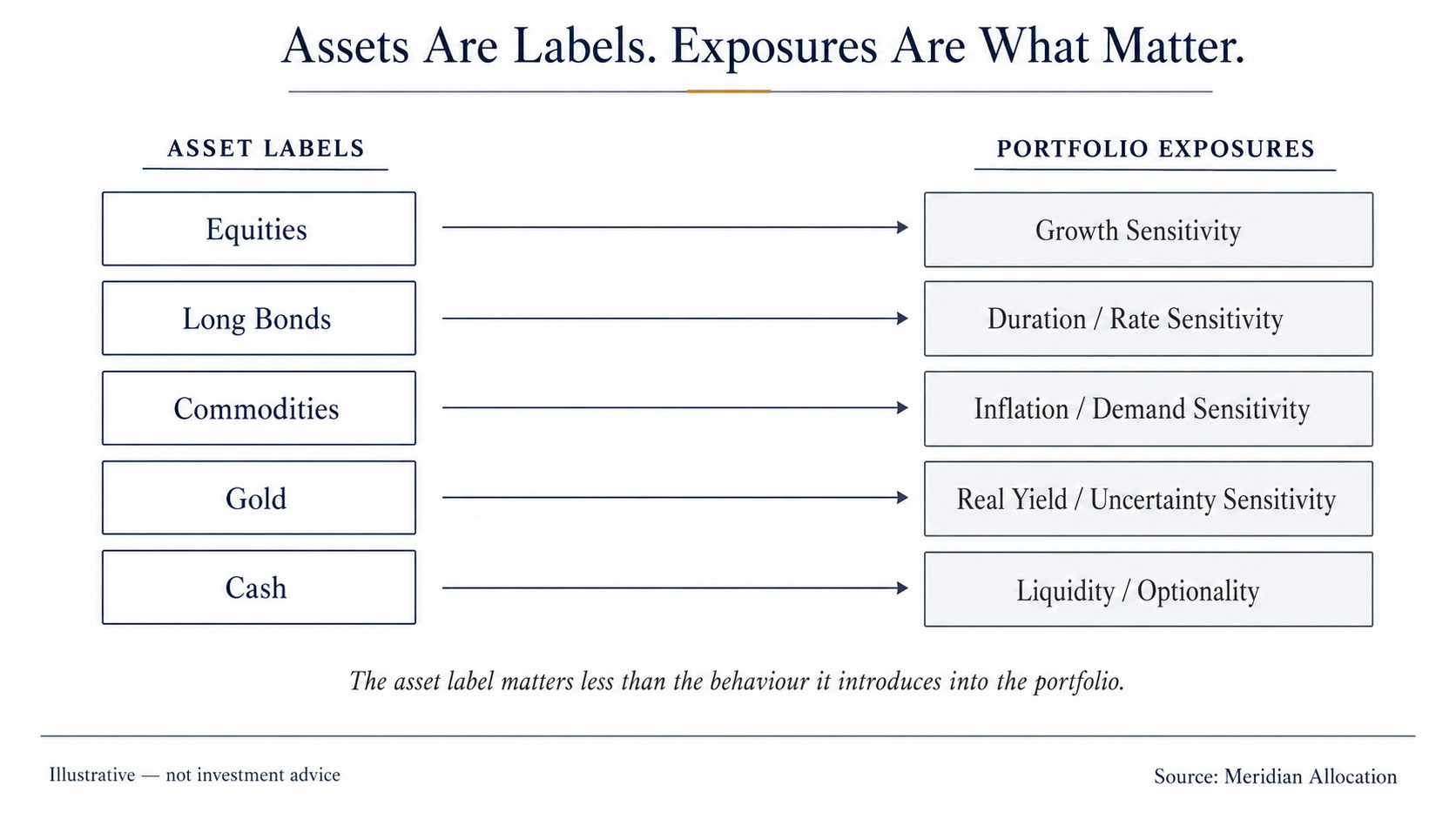

The asset label matters less than the behaviour the asset introduces.

Equities are not just “stocks.”

They are often growth-sensitive exposure.

Long-duration bonds are not just “safe assets.”

They are rate-sensitive and inflation-sensitive exposures.

Commodities are not just an “inflation hedge.”

They are often demand-sensitive, supply-sensitive, and regime-dependent exposures.

Gold is not just a defensive asset.

Its role can shift depending on real yields, currency confidence, inflation uncertainty, and stress conditions.

Cash is not simply idle capital.

It can be a liquidity reserve, a volatility dampener, and an option on future opportunity.

This is how institutional thinking differs from ticker-level thinking.

The relevant question is not only:

Do I own this asset?

It is:

What exposure am I adding?

And just as importantly:

What exposure am I already over-reliant on?

Many portfolios appear diversified because they own different asset classes. But at the exposure level, they may be more concentrated than they look.

That distinction becomes critical when the macro environment changes.

Why Role Matters More Than Ownership

In a serious portfolio, each allocation should have a job.

Some exposures are intended to participate in growth.

Others are intended to provide defense.

Some are designed to respond to inflation pressure.

Some exist to preserve liquidity.

Some are useful only under specific conditions and should not be treated as permanent solutions.

This is where many self-directed portfolios become loose.

An asset is purchased because it seems attractive, but its role is never defined. Later, when the environment changes, the investor does not know whether to hold it, reduce it, increase it, or replace it.

The portfolio lacks role clarity.

Role clarity matters because the same asset can behave differently across regimes.

Bonds, commodities, gold, and cash can all play useful roles.

But those roles change with the regime.

A diversifier in one environment can become ineffective, secondary, or even vulnerable in another.

The asset has not changed.

The environment has.

That is why the question should not be:

Do I own bonds, commodities, gold, or cash?

The better question is:

What role should this exposure play in the current regime?

Why Institutions Care About Risk Budgets and Portfolio Behaviour

Institutional allocators care deeply about risk because portfolios have to survive more than one environment.

A portfolio that performs well only in favourable conditions is not robust. It is conditionally successful.

That distinction matters.

Risk is not just volatility on a report. It is the possibility that the portfolio becomes structurally exposed to the wrong environment.

This can happen even when the holdings appear diverse.

Correlations can shift.

Assets can begin moving together.

Diversifiers can stop diversifying.

Drawdowns can become larger than expected.

Liquidity can matter more than expected.

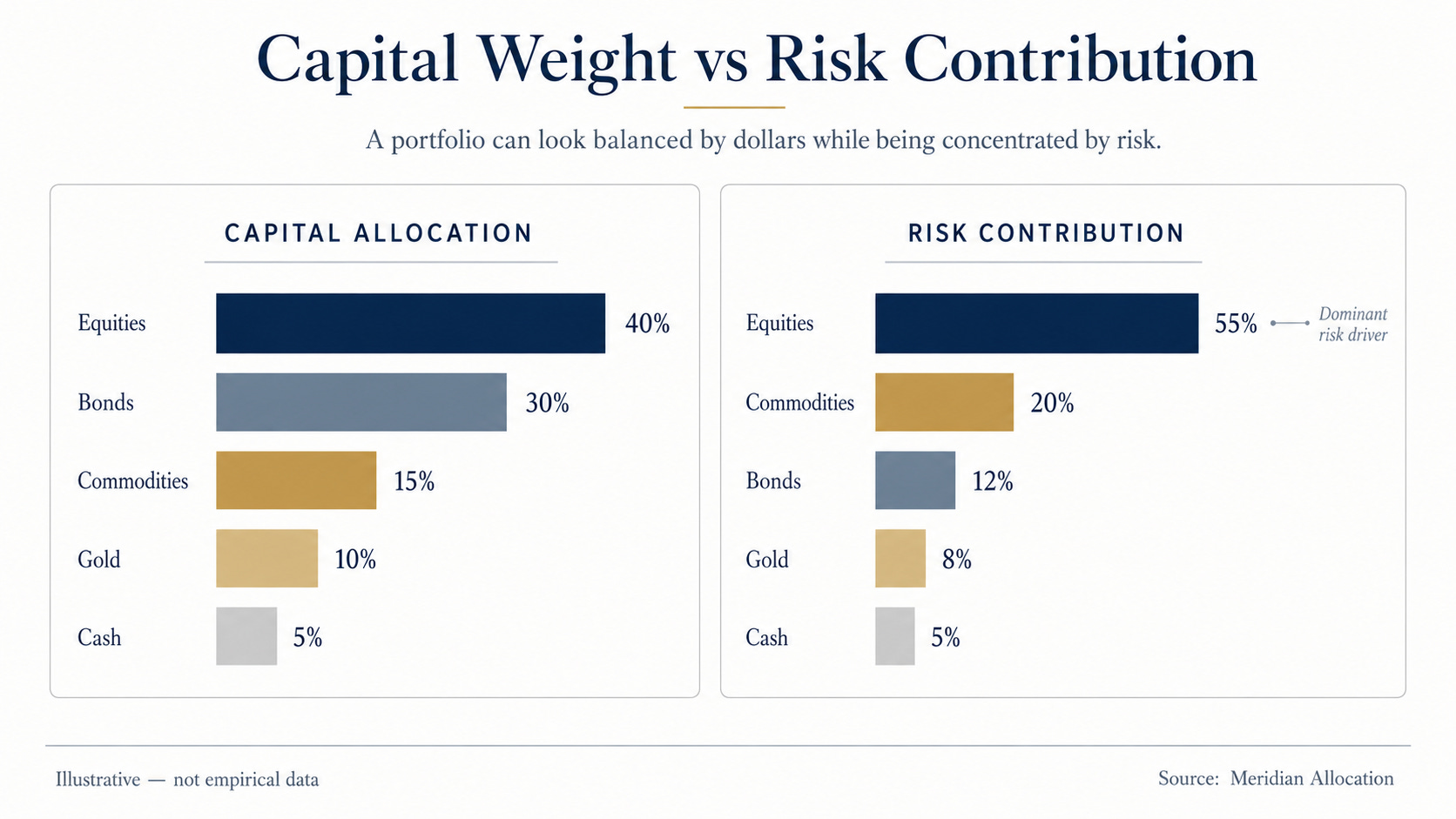

This is why institutions think in terms of risk budgets.

A risk budget asks how much risk should be allocated to each exposure, not just how much capital.

A 20% allocation to one asset may contribute more portfolio risk than a 40% allocation to another if it is more volatile or more correlated with the rest of the portfolio.

Capital weight and risk contribution are not the same thing.

A portfolio can look balanced by dollars while being unbalanced by risk.

That is why serious allocation requires portfolio-level thinking. The task is not to maximize exposure to every attractive idea. The task is to build a structure that can remain defensible across changing conditions.

Why This Matters for Serious Self-Directed Investors

This way of thinking is not only relevant to pension funds, endowments, or large institutions.

A serious self-directed investor can use the same logic at a practical level.

The goal is not to imitate a large fund.

The goal is to adopt a more disciplined allocation mindset.

It means defining the role of each exposure before adding it.

It means thinking about the macro environment rather than only the asset story.

It means recognizing that allocation is the main decision, not an administrative detail after asset selection.

It means asking whether the portfolio is built around structure or simply accumulated conviction.

This shift is subtle but powerful.

Most investors spend too much time asking what to buy.

They spend too little time asking how much exposure they should carry, what role that exposure plays, what risk it introduces, and whether the current environment supports it.

That is the institutional lesson that matters most.

Not sophistication for its own sake.

Structure.

Where Meridian Allocation Fits

Meridian Allocation is built around this structural view of portfolios.

It is not a stock-picking service, a stream of trading calls, or a reaction to every market headline.

Meridian exists for investors who want a disciplined way to allocate capital across broad exposures as macro conditions change.

The framework classifies the broad macro regime, translates that environment into long-only ETF portfolio weights, and applies risk controls as conditions evolve.

The premise is simple: asset behaviour changes with the environment.

Meridian’s focus is exposure, structure, and risk-aware allocation.

Serious portfolio construction is not mainly about owning good assets.

It is about allocating capital deliberately across exposures, roles, and risks.

An asset can be attractive and still be the wrong allocation.

A portfolio can hold many assets and still be structurally concentrated.

A strategy can look diversified and still depend on one environment persisting.

Institutional allocators are not always right.

But they usually understand something many investors miss:

The portfolio is the decision.

Not the ticker.

Not the story.

Not the forecast.

The structure.

If this way of thinking fits how you invest, follow the publication and join the Meridian waitlist.

Because serious allocation begins when capital stops being assigned to ideas and starts being assigned to roles.