Why Commodities Are Not a Universal Inflation Hedge

Commodities are often treated as a straightforward inflation hedge.

When inflation rises, add commodities.

When inflation falls, reduce them.

The logic sounds simple.

It is also incomplete.

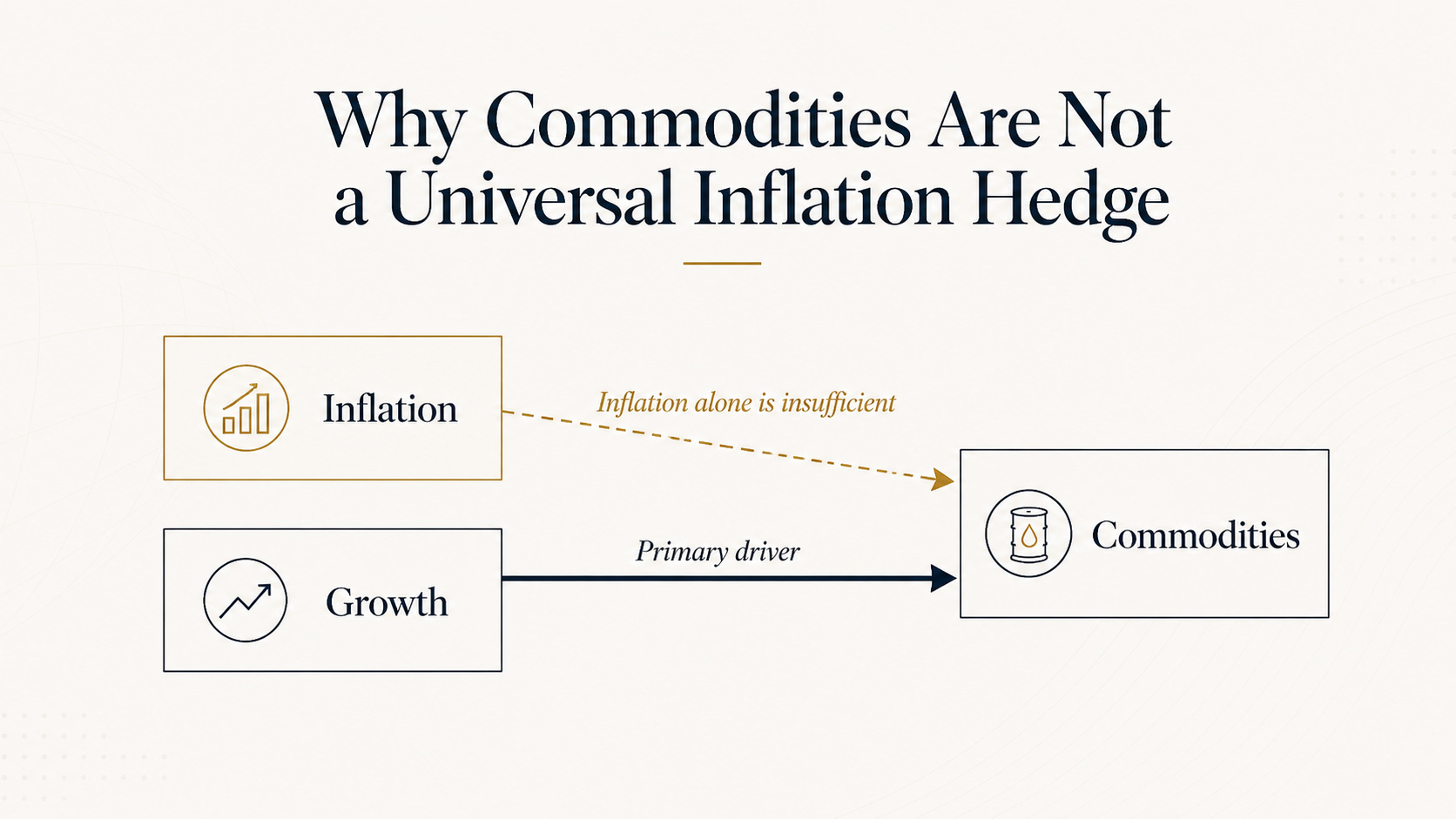

Commodities are not a universal inflation hedge. They are a regime-dependent exposure.

The Common Investor Mistake

Many investors reduce commodities to a single function:

inflation hedge

Within that framing, commodities are treated as a permanent portfolio sleeve.

This is a simplification.

It assumes that all inflation is similar.

It assumes that demand conditions do not materially affect commodity performance.

It assumes that the relationship between inflation and commodities is stable.

None of these assumptions consistently hold.

Investors expect commodities to protect portfolios during inflationary periods.

The problem is that inflation alone does not determine whether that expectation is justified.

Why Inflation Alone Is Not Enough

Inflation is not a single, uniform phenomenon.

It can emerge from different sources:

strong demand

constrained supply

monetary expansion

policy shocks

Commodity performance depends not just on whether inflation is rising, but on why it is rising.

In particular, the growth backdrop matters.

Commodities are fundamentally tied to real economic activity. Their demand is closely linked to:

industrial production

construction activity

transportation demand

broader economic expansion

If inflation rises alongside strong growth, demand for commodities is often robust.

If inflation rises while growth weakens, demand conditions can deteriorate even as prices remain elevated.

Many investors only discover this after commodities fail to protect a portfolio in an inflationary environment they assumed would be supportive.

Inflation is a signal.

Commodity performance depends on the environment behind that signal.

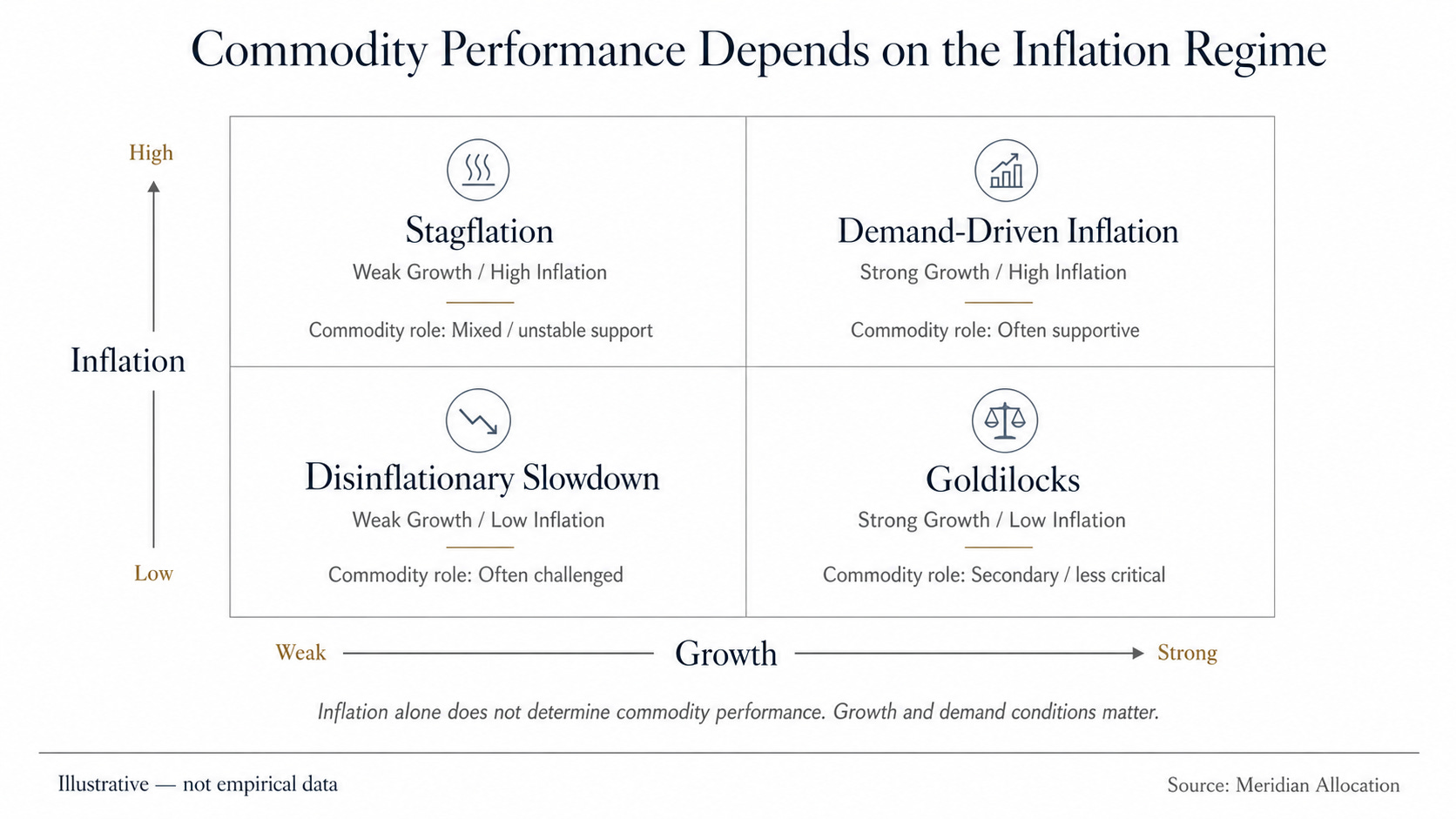

Different Inflation Environments Produce Different Outcomes

The key distinction is not inflation versus no inflation. It is inflation with strong demand versus inflation with weakening demand.

Rising Growth + Rising Inflation

This is often the most supportive environment for commodities: demand is strong, activity is expanding, and pricing power can be sustained.

In this regime, commodities can perform well because both price and volume dynamics are aligned.

This is the environment most investors implicitly assume when they think of commodities as an inflation hedge.

Weak Growth + Rising Inflation

This is a more complex environment.

Inflation may remain elevated due to supply constraints or prior shocks.

But demand is no longer expanding.

In this regime:

industrial demand may weaken

consumption may slow

inventories may build

Commodities can become less responsive to inflation, even if headline inflation remains high.

Prices may be supported in the short term but lack sustained momentum.

This is often where the “inflation hedge” narrative breaks down.

Disinflationary Environments and Unstable Demand Conditions

Outside these clearer regimes, commodities can also behave inconsistently when disinflation, unstable demand, or policy uncertainty remove directional support. In those environments, the inflation-hedge label often becomes less useful than investors assume.

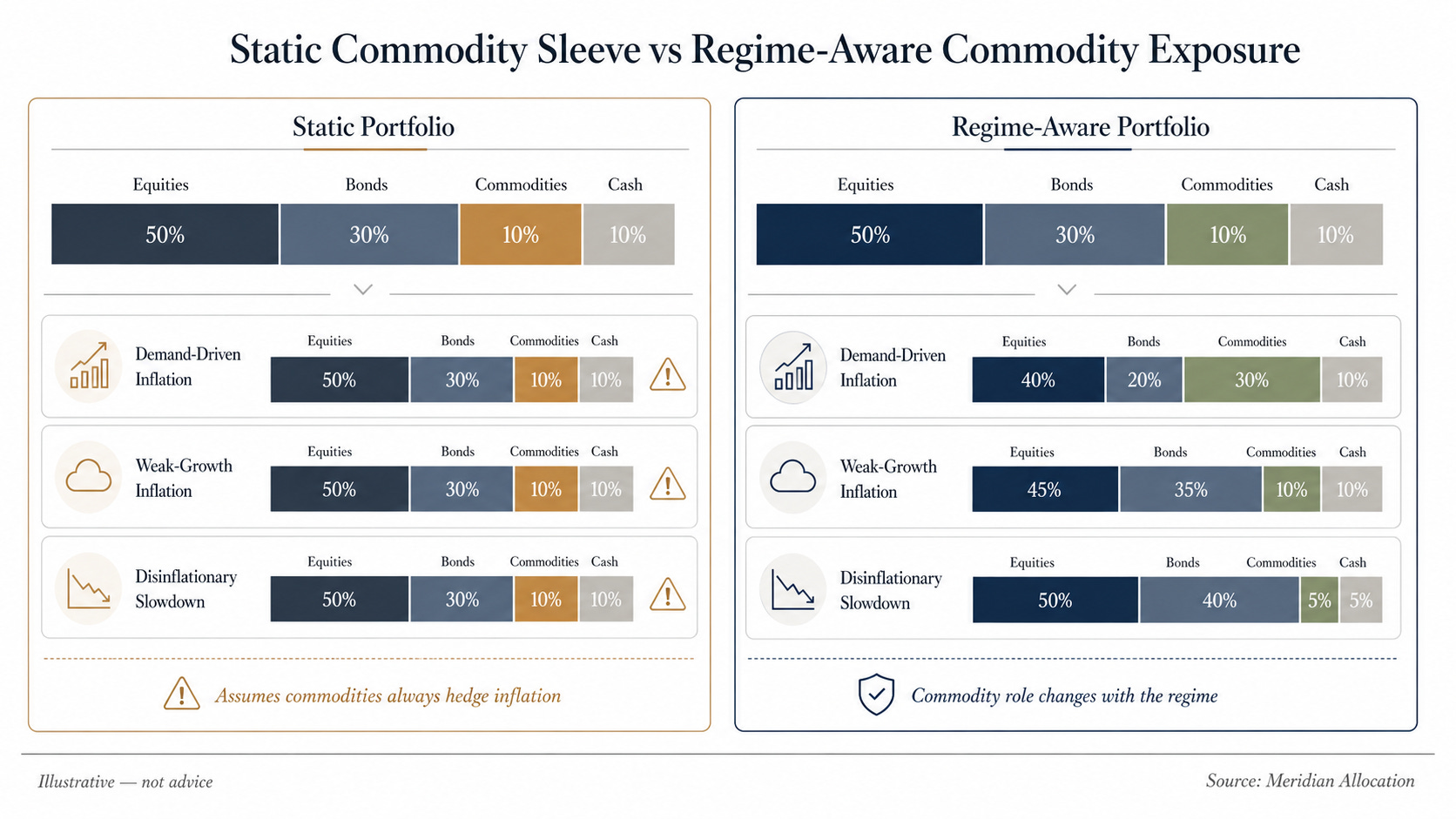

Why Static Diversification Gets This Wrong

Static portfolios treat commodities as a permanent sleeve.

Regime-aware portfolios treat them as a conditional tool.

Static portfolios often assign commodities a fixed role.

They are included as an “inflation hedge” alongside equities and bonds.

This implicitly assumes:

inflation is the dominant driver of commodity returns

the relationship between inflation and commodities is stable

commodity exposure provides consistent diversification benefits

The problem is that commodity behaviour is regime-dependent, not constant.

A static allocation treats commodities as if they perform the same function across all environments.

In reality, their role shifts with:

growth conditions

demand strength

policy direction

supply constraints

When those assumptions break, diversification weakens.

This is not a failure of commodities.

It is a failure of how they are being used within the portfolio.

Asset Label vs Portfolio Role

There is an important distinction between an asset and its role.

Commodities are an asset class.

But their portfolio role is not fixed.

In some regimes, they act as inflation-sensitive growth exposure

In others, they may behave more like volatile, demand-dependent assets with limited diversification benefit

The difference depends on the macro environment.

Treating commodities purely as an “inflation hedge” ignores this distinction.

It substitutes a label for a structural understanding.

This is the same mistake seen in other areas of portfolio construction:

assuming bonds always hedge equities

assuming correlations are fixed

In each case, the issue is not the asset.

It is the assumption of permanence.

What This Means for Allocation

The implication is not that commodities should be avoided.

It is that they should be treated as conditional exposures.

The relevant question is not:

Should commodities be in the portfolio?

It is:

Is the current environment supportive of their role?

In practice, this means:

increasing commodity exposure when inflation is supported by strong demand and growth

being more cautious when inflation is present but demand conditions are weakening

recognizing when commodities are likely to behave as risk assets rather than diversifiers

This is not about predicting short-term prices.

It is about aligning exposure with the broader environment, because that alignment determines whether an asset contributes to resilience or fragility.

Instead of asking whether inflation is rising, the more useful question is what type of environment is driving it.

That distinction determines whether demand is supportive, whether pricing power is sustainable, and whether commodities are aligned with the broader macro regime.

Commodities become more useful in portfolio construction when they are treated as conditional exposures rather than static labels.

In some environments, commodities can provide meaningful support.

In others, they may offer limited protection or behave more like traditional risk assets.

The issue is not whether commodities are “good” or “bad.”

It is whether the environment justifies their role.

Static diversification assumes stability.

Adaptive allocation recognizes change.

Commodities are not a universal inflation hedge.

They are a macro-sensitive exposure whose role changes with the regime.