Why Drawdown Control Matters More Than Returns

Drawdowns Are the Real Risk

Investors often talk about market volatility as if it were the primary danger.

It is not.

Volatility describes movement.

Drawdowns describe damage.

A portfolio that fluctuates but recovers quickly rarely destroys long-term outcomes. The real threat emerges when losses become deep or prolonged enough that the portfolio’s ability to recover is compromised.

Thus, most investment failures are not caused by poor average returns.

They are caused by losses that are too large to recover from within a reasonable timeframe.

Drawdowns are defined not only by depth, but by duration.

A portfolio that recovers in months is fundamentally different from one that requires years.

The Mathematics of Recovery

The problem with drawdowns is structural.

Losses compound asymmetrically.

The asymmetry becomes obvious when the recovery required after losses is examined.

The deeper the drawdown, the more recovery depends on time rather than allocation skill.

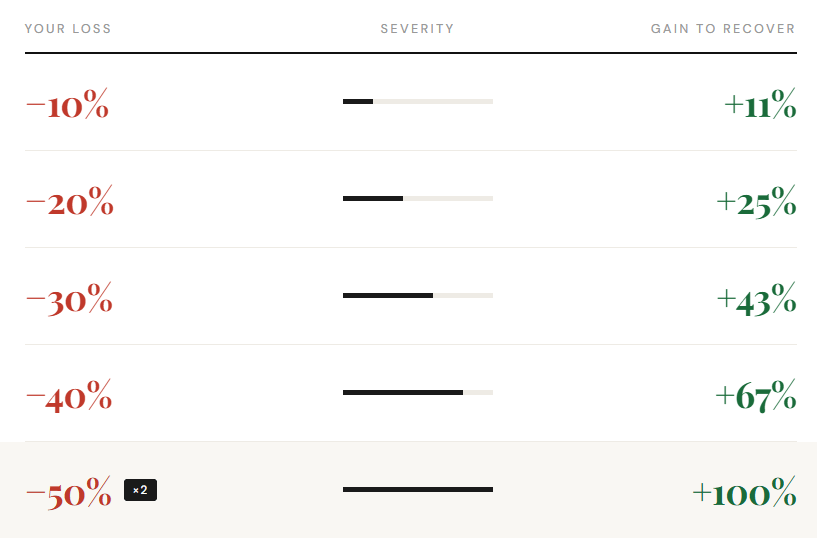

A portfolio that loses 50% must double simply to return to its starting point.

Once drawdowns exceed 40–50%, recovery becomes primarily a function of time rather than portfolio construction.

This is why so many portfolios quietly break.

They become overly dependent on favorable environments to repair past damage.

A proper risk process can avoid entering this position in the first place.

Why Most Portfolios Ignore This

In strong markets, drawdowns appear distant and irrelevant.

Growth is strong, and the dominant conversation becomes return maximization.

During these periods, many investors optimize for the wrong variable.

They ask:

How can I increase returns?

The more important question is:

What happens if the environment changes?

A portfolio that performs well only when conditions remain favorable is not robust.

It is simply untested.

Frankly, any portfolio can be a winning portfolio given the right conditions.

Drawdowns Are Where Strategy Is Revealed

Every strategy appears coherent during expansionary periods.

Risk management only becomes visible when conditions deteriorate.

This is when structural weaknesses tend to surface.

Portfolios overconcentrated in a single asset class have nowhere to hide. Strategies built on historical correlations find that those relationships break down precisely when they’re needed most. Leverage that assumed stable liquidity becomes a liability overnight. And allocations that were never designed for contraction simply weren’t built for the environment they’re now operating in.

None of these problems are obvious when markets rise.

They emerge during stress.

By that point, adjustment becomes difficult.

Risk Management Is About Survival

A portfolio that survives adverse environments keeps something extremely valuable:

time.

Time allows compounding to work.

Time allows opportunities to reappear.

Time allows capital to participate in future regimes.

Portfolios that suffer severe drawdowns often lose this advantage. The recovery process can take years, sometimes decades, and during that period the portfolio is effectively stalled.

This is why risk management should be viewed as a precondition for long-term returns, not a constraint on them.

The Role of De-Risking

One of the most difficult decisions in portfolio management is reducing risk during deteriorating environments.

It is psychologically uncomfortable.

Reducing exposure during uncertainty often feels premature. Waiting for confirmation often feels safer.

But the cost of waiting is that losses compound while decisions are delayed.

Risk management systems therefore tend to rely on rules rather than judgment.

Not because judgment is ineffective, but because conditions that require de-risking are usually the same conditions where judgment becomes most clouded and unreliable.

Capital Preservation Is Structural

A robust allocation framework must assume that unfavorable regimes will occur.

Recessions arrive.

Liquidity tightens.

Correlations change.

None of these are anomalies.

They are a part of how markets function.

The objective of risk management is not to avoid all losses. That would be impossible.

The objective is to prevent losses from reaching levels that permanently impair the portfolio’s trajectory.

If that objective is achieved, long-term compounding can continue.

Over long horizons, the portfolios that compound successfully are rarely the ones that pursued the highest returns.

They are the ones that survived.

Meridian Allocation is a rules-based macro allocation framework designed to prioritize capital preservation, regime consistency, and controlled drawdowns.